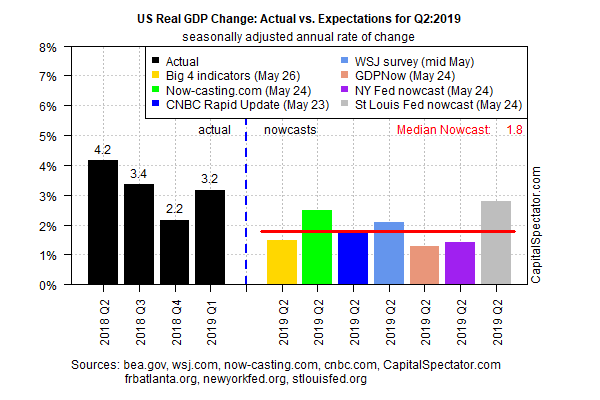

1st Quarter 2019:

The US economy expanded by an annualized 3.10% in the 1st quarter of 2019, unrevised from the second estimate issued last month and following a 2.20% expansion in the previous 3 months. Upward revisions to nonresidential fixed investment, exports, state and local government spending, and residential fixed investment were offset by downward revisions to personal consumption expenditures and inventory investment and an upward revision to imports.

GDP Growth Rate in the US averaged 3.22 percent from 1947 to 2019, reaching an all time high of 16.70 percent in the first quarter of 1950 and a record low of -10 percent in the first quarter of 1958.

2nd Quarter 2019:

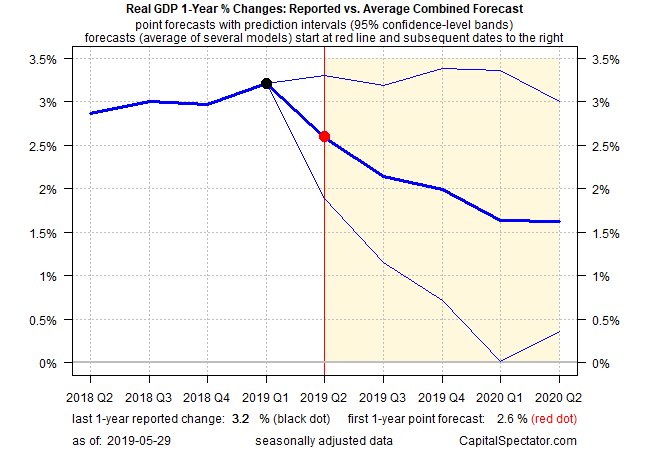

At this point, using data published to date,

it appears that the US is headed for a

period of slower growth.

it appears that the US is headed for a

period of slower growth.

The economy is expected to grow by 1.80%

in 2nd quarter based on the median for a

set of GDP estimates compiled by

The Capital Spectator.

in 2nd quarter based on the median for a

set of GDP estimates compiled by

The Capital Spectator.

Aside from GDP estimates, one thing that is

affecting economic expectations is the

deepening inversion of the Treasury

yield curve, which is widely viewed as

an indicator of elevated recession risk.

affecting economic expectations is the

deepening inversion of the Treasury

yield curve, which is widely viewed as

an indicator of elevated recession risk.

Looking beyond the yield curve, however,

suggests that US recession risk remains

low.

suggests that US recession risk remains

low.

Economic growth remains on track for a slower

growth in the second quarter vs. the first one,

based on a set of now-casts. Although the

current estimates suggest that the economy

has low risk to fall into a recession in the

immediate future, output for the April to June

period seems to be at risk of decelerating to

the softest pace in more than two years.

growth in the second quarter vs. the first one,

based on a set of now-casts. Although the

current estimates suggest that the economy

has low risk to fall into a recession in the

immediate future, output for the April to June

period seems to be at risk of decelerating to

the softest pace in more than two years.

The economy is expected to expand 1.80% in Q2 2019, based on the median for a set of GDP estimates compiled by "The Capital Spectator". If today's median Q2 estimate is correct, the growth will show a substantially softer gain compared with 1st Quarter's strong 3.20 percent increase.

Aside from GDP estimates, Treasury yield curve is being widely viewed as an indicator of elevated recession risk. This spread ticked deeper into negative territory on May 28, when the 3-months Treasury yield exceeded the 10 year yield by 12 basis points , the deepest negative spread since the year 2007.

"The drop of the US Treasury yield is an indicator of growing uncertainty," Lena Komileva, chief economist at G Plus Economics, told Bloomberg. "It's quite clear now that we are past that cyclical peak for earnings and the cyclical trough in credit spreads." She added that Treasuries are "going to be very well-supported here."

Looking beyond the yield curve, however, suggests that US recession risk remains low. Perhaps the leading risk factor at the moment is the escalating US-China trade conflict.

Wednesday's revised point forecast anticipates that the year over year rate of growth will decelerate for several quarters.

The crucial question in the days and weeks ahead: Will incoming data materially change the outlook? Based on estimates and the previous data, these updates are expected to show that recession risk remains quite low. But as growth slows down, any downside surprises will surely negative effects on coming quarters too. The US, in short, seems heading towards a challenging 2nd half in 2019.

No comments:

Post a Comment